Fashion companies will face economic headwinds, technology shifts, and an evolving competitive landscape in 2024. However, shifting consumer priorities will continue to offer opportunities. The most prominent sentiment among fashion industry leaders at the moment is uncertainty, reflecting the prospect of subdued economic growth, persistent inflation, and weak consumer confidence. Against this backdrop, businesses will be challenged to identify pockets of value and unlock new drivers of performance.

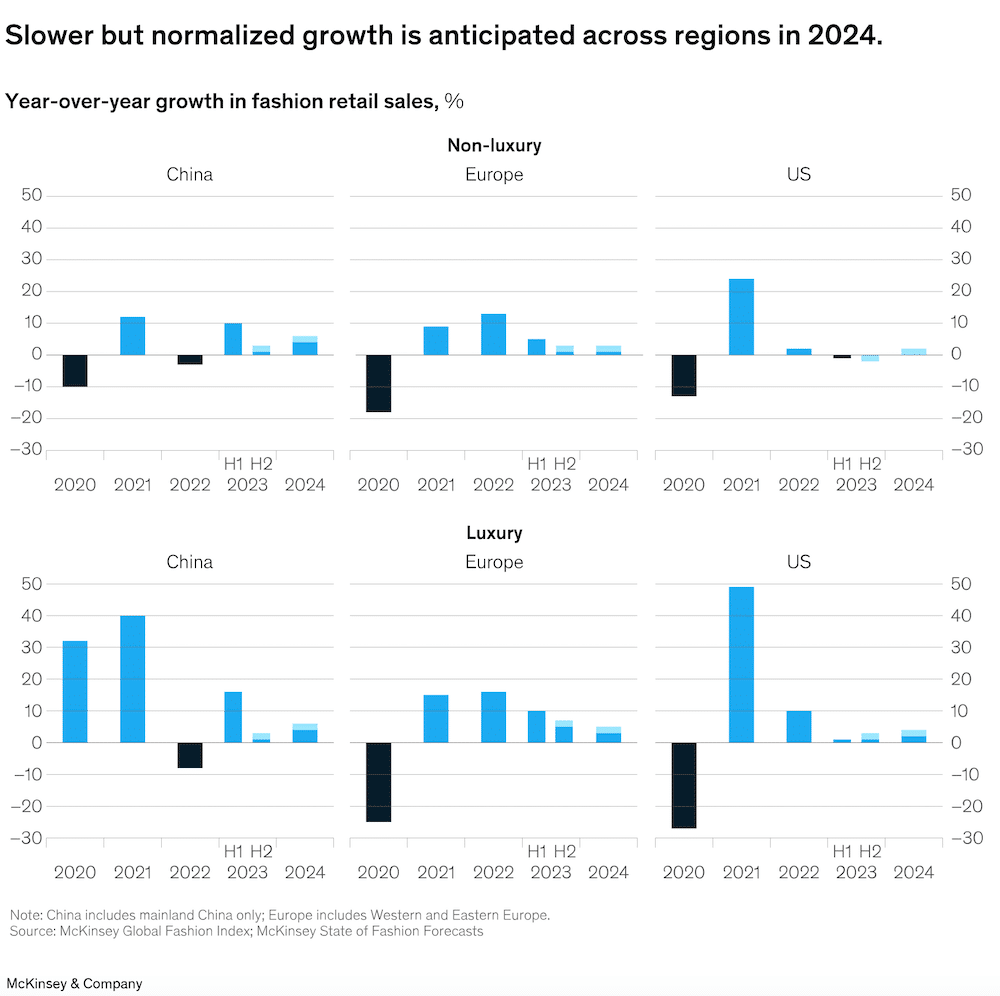

According to McKinsey’s analysis of fashion forecasts, the global industry will post top-line growth of 2 to 4 per cent in 2024 (exhibit), with regional and country-level variations. Once again, the luxury segment is expected to generate the biggest share of economic profit. However, even there, companies will be challenged by the tough economic environment. The segment is forecast to grow globally by 3 to 5 per cent, compared with 5 to 7 per cent in 2023, as consumers rein in spending after a post-pandemic surge. European and Chinese growth is set to slow, while US growth is expected to pick up after a relatively weak 2023, reflecting the slightly more optimistic outlook there.

Beyond luxury, growth of 2 to 4 per cent is predicted for the year ahead, in line with the probable outcome in 2023. The European market will likely expand by just 1 to 3 per cent, compared with 5 per cent in the first half of 2023 and 1 to 3 per cent in the second half. Slumping consumer confidence and declining household savings are expected to be the most probable causes of restrained spending. In the United States, nonluxury sector growth of 0 to 2 per cent is forecast. China is expected to be similarly challenged amid 4 to 6 per cent growth, which is a slight uptick from the end of 2023 but slow when considered on a historical basis.

Uncertainty in the face of headwinds

With conflicts in Europe and the Middle East and strained international relations elsewhere, geopolitics is the number-one concern for fashion industry executives going into 2024, followed by economic volatility and inflation. Some 62 per cent of executives in this year’s survey, conducted in September, cite geopolitical instability as the top risk to growth. Economic volatility is cited by 55 per cent and inflation is mentioned by 51 per cent (compared with 78 per cent last year). The global average headline rate of inflation is predicted to moderate to 5.8 per cent—still high on a historical basis—from 6.9 per cent in 2023.

Uncertainty within the industry reflects the broader economic situation, albeit with regional divergence. Going into 2024, pressure on household incomes is expected to dampen demand for apparel and prompt trading down across categories. Still, there are geographic outliers that may offer comfort. One is India, where consumer confidence hit a four-year high in September 2023. India-based executives are more optimistic than those in Western countries, with 85 per cent of respondents to McKinsey’s Global Economics Intelligence survey saying that conditions have improved in the past six months. China’s economy is facing challenges, but the country’s consumers show a higher intent to shop for fashion in 2024 than consumers in both the United States and Europe.

McKinsey – The State of Fashion 2024 – Ten Themes for 2024

To prepare for challenges and be alert to opportunities, leading fashion companies will likely prioritize contingency planning for the coming year. A key theme will be companies keeping a firm grip on costs and inventories while driving growth by precisely managing prices. Brands and suppliers can expect an increasingly competitive environment. But they will also have opportunities, with consumers discovering new styles, tastes, and priorities—all presenting routes to value creation. As previously done, this year’s report highlights ten emerging themes that will be high on leadership agendas.

- Global economy:

- Fragmented future. In 2024, the global economic outlook will continue to be unsettled, as financial, geopolitical, and other challenges weigh on consumer confidence. Fashion markets in China, Europe, and the United States will likely face headwinds, some of which reflect individual regional dynamics. Suppliers, brands, and retailers may need to bolster contingency planning and manage uncertainty.

- Climate urgency. The frequency and intensity of extreme weather-related events in 2023 mean the climate crisis is an even more urgent priority than in previous years. With physical and transition risks rising across continents, the industry must not delay in tackling emissions and building resilience in supply chains.

- Consumer shifts:

- Vacation mode. Consumers are gearing up for the biggest year of travel since before the pandemic. But a shift in values means expectations are evolving, even as shopping remains a priority. Brands and retailers should refresh distribution and category strategies to reflect the new reality.

- The new face of influence. It’s time for brand marketers to update their influencer playbooks, as a new guard of creative personalities wins fans. Working with opinion leaders in 2024 will require a different type of partnership, an emphasis on video, and a willingness to loosen the reins on creative control.

- Outdoors reinvented. Technical outdoor clothing and “gorpcore” are in demand as consumers embrace healthier lifestyles. In 2024, more outdoor brands are expected to launch lifestyle collections. At the same time, lifestyle brands will likely embed technical elements into collections, blurring the lines between functionality and style.

- Fashion system:

- Generative AI’s creative crossroads. After generative AI’s (gen AI) breakout year in 2023, more use cases are emerging across the industry. Capturing value will require fashion players to look beyond automation and explore gen AI’s potential to enhance the work of human creatives.

- Fast fashion’s power play. Fast-fashion competition is set to be fiercer than ever. Challengers, led by Shein and Temu, are bringing new tactics on price, customer experience, and speed. Success for disruptors and incumbents could hinge on adapting to new consumer preferences while navigating the regulatory agenda.

- All eyes are on the brand. Brand marketing is expected to be back in the spotlight as the fashion industry manages a switch away from performance marketing. Brands may benefit from forging emotional connections with consumers – derived from ever more sophisticated personalisation technology, as marketers rewrite playbooks to emphasise long-term brand building.

- Sustainability rules. The era of fashion industry self-regulation is drawing to a close. Across jurisdictions, new rules will have significant effects on both consumers and fashion players. Brands and manufacturers may consider revamping business models to align with the changes ahead.

- Bullwhip snaps back. Shifts in consumer demand have created a “bullwhip effect,” by which order volatility reverberates unpredictably through supply chains. Suppliers will likely face pressure as brands and retailers focus on transparency and strategic partnerships.

Looking ahead

As the industry continues to be challenged by geopolitical and economic headwinds, fashion leaders in 2024 will look to strike a careful balance between managing uncertainty and seizing opportunities. With cost-saving tactics mostly exhausted, companies may focus on growing sales, underpinned by new pricing and promotion strategies. Across the industry, net intent to raise prices is more than 50 per cent, according to the BoF–McKinsey Executive Survey. At the same time, reduced cost pressures could provide a potential boost to performance.

As climate change brings increasingly extreme weather events and global temperatures rise, the coming year is likely to mark a heightened industry focus on environmental, social, and governance issues. Our survey shows that the topic is seen as both the number-one priority and number-one challenge for industry executives. The most successful companies will find a balance between sustainability initiatives, risk management, and commercial imperatives.

In an uncertain world, consumer discretionary spending will be weighted toward trusted categories and brands. Hard luxury goods—jewellery, watches, and leather—will likely be in demand, reflecting their potential investment value in tough economic times. Consumers are expected to travel more and continue spending more time outdoors. And they prefer emotional – uniquely private and personalised – connections and authenticity over celebrity endorsements, as that’s where the ROI is.

All told, executives are bracing for a strategically complex year ahead. To counter uncertainty, leading companies will prepare for a range of outcomes. The most successful will become more resilient, better equipped to manage the challenges, and ready to accelerate when the storm clouds begin to clear.