Ecommerce platforms, companies that produce packaged goods for consumers, and how consumers act have all undergone major transformations over the past five years. These changes have not been uniform, leading to shifts in how these entities interact, resulting in a growing sense of unease as the battle for consumer attention and importance intensifies. Those in the know appreciate that essential consumer relevancy is crucial to stand a chance of any success from here on.

Should we consider reevaluating these relationships? The shift in these dynamics is partly due to the turbulent times we find ourselves in, but it also shows a desire to embrace innovation and adopt new technologies. As these companies shift their strategies from established methods, their decisions have affected their internal operations and redefined their connections with suppliers and buyers.

However, what does this imply for what lies ahead? Ultimately, it’s the consumers who have the upper hand, so are ecommerce and CPG companies keeping up with the evolving tastes and more importantly relevancy, of their consumers? And would more cooperation, rather than individual strategies, be the key to repairing these relationships?

CPG companies have become more accessible

Consumer packaged goods (CPG) firms are leveraging technology to bridge the gap and establish a bond with their customers. Numerous have embraced direct-to-consumer (D2C) strategies, which extend beyond just online platforms to include subscription services, social selling, and temporary pop-up shops, and are constantly discovering innovative methods to influence pricing, enhance brand positioning, streamline the supply chain, and gather consumer insights.

the advent of AI, especially the focus on machine learning hyper-personalisation, means that each consumer now identifies as unique from the rest of your database. No one is naive enough to no longer appreciate that’s where you keep track of them and what they like. You need only watch data piracy scandals on the news to appreciate it happening and, by implication, the value of that data to criminals and retailers alike. They now have an appreciation of their worth and likewise expect a return on their provision of data, to be reciprocated by the ecommerce retailer as a consequence.

CPG firms have faced the challenge of sustaining production amidst persistent disruptions, necessitating the reduction of expenses and the implementation of growth strategies. They have concentrated on making their supply chains more adaptable and efficient, scrutinizing their ingredients and formulations to lower expenses and increase sustainability, as well as reevaluating the sizes of their products, the range of offerings, and the design of their packaging to boost profitability. In their quest to maintain sales levels, they are looking into alternative retail outlets beyond the traditional major grocery stores and ecommerce sites, including convenience stores, value stores, and members clubs, and are also adapting to the increasing influence of larger retailers.

Brands are not important in 48% of purchase decisions, putting CPG companies at a disadvantage

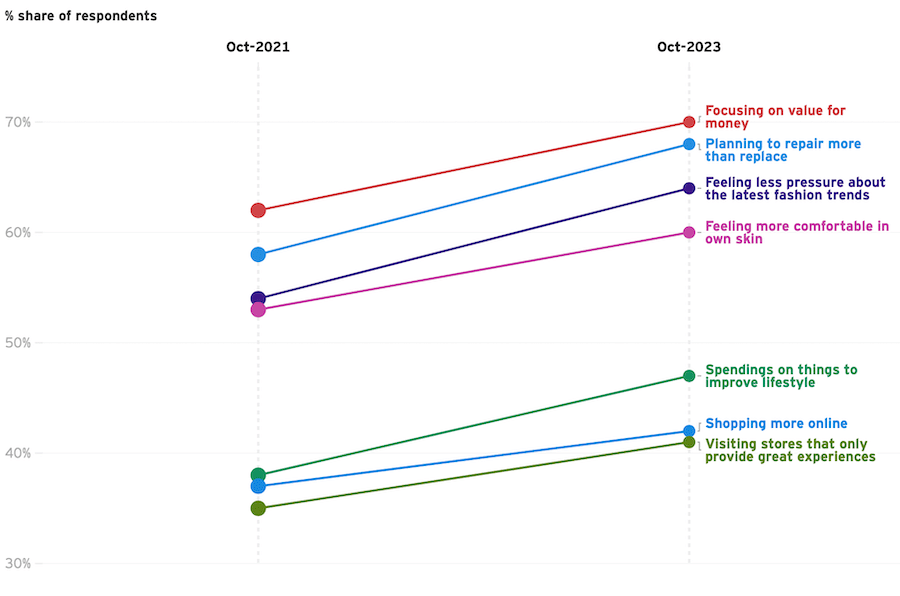

Shoppers are now more discerning and are making purchases in a manner that reflects their unique objectives and principles, hence the need for hyper-personalisation. They are significantly more conscious of prices; they are purchasing fewer items and opting for second-hand shopping more frequently. A growing number are turning to online shopping, arranging for deliveries at their homes, and visiting physical stores less often. More and more, they are engaging with social media platforms throughout the day and are better educated than before about the products they buy – this includes knowing the ingredients a company uses in its products, how it manages its workforce or the size of its environmental impact.

Essential consumer relevancy and values are changing significantly

Shopping preferences and choices are evolving, moving away from previously popular brands. Nowadays, branded items are appearing in smaller quantities, with 74% of shoppers noticing a trend towards shrinkflation. Additionally, 50% would consider switching to a different brand if it offered higher quality. There’s a growing openness to private label brands, with 41% already making the switch.

Brands are losing their significance in 48% of buying decisions, putting consumer goods companies at a disadvantage. New dynamics of power are taking shape. Consumer goods companies and retailers are now engaging in a different type of relationship with consumers and with each other.

The old straightforward model was: that companies produced brands; retailers sold them in their stores; and consumers purchased them. This was the norm for many years. However, with consumers placing more emphasis on value and price, there’s a noticeable decline in brand loyalty, especially for non-luxury items, and an increased focus on what retailers can offer directly. These shifts are amplifying a classic struggle for consumer goods companies.

They’ve always strived to convince consumers that their brands justify a higher price tag and to encourage retailers to display them prominently. However, retailers now have more control over their display areas, making sure each product competes for its spot, especially with the rise of private label products they aim to sell. Yet, all this overlooks the crux of the problem, which is to understand what each consumer desires, rather than aiming to cater to broad market segments.

Yet, all this overlooks the true essence, which is to understand what each consumer desires, rather than aiming to cater to broad market segments, a strategy that has been followed for the past few centuries and is almost defunct now.

Shopping is fragmenting, making value elusive

In certain areas of the CPG relationship, it seems the balance of power is shifting more towards the retailer. However, they should not get too carried away with this shift. In an era where online marketplaces, peer-to-peer networks, subscription services, and social media are reshaping the way we shop, customers are not merely moving away from brands they’ve relied on in the past; they’re also finding traditional shopping experiences less appealing.

Moreover, the way people shop online is becoming more diverse and intricate, with 29% of shoppers now purchasing directly from social media ads, reducing the necessity for a brick-and-mortar store. Yet, 38% still prefer to buy online but then pick up their purchases in-store, making a physical store essential. While some retailers are experiencing a newfound sense of control, the rapid growth of online shopping is posing challenges to their profit margins and introducing more complexity into their business strategies. (Look how the stats still offer data in terms of a lump of customers, as they are not able to reflect individuals’ ever-changing relevancy, taste and needs).

As the shopping journey broadens across various platforms, the task – or chance – for both CPG companies and retailers is to offer a shopping experience that customers appreciate, without the added expense of providing that experience making it unviable. At the same time, they must look past their usual methods of measuring success and KPIs, seeking ways to add value to their business that may not yield immediate profits but are crucial for long-term viability, such as gathering first-party data and fostering consumer trust.

The AI opportunity

There are countless methods to leverage AI to transform existing obstacles into assets. The strategic application of AI is becoming a key factor in driving expansion and enhancing profit margins. AI can assist in predicting upcoming customer demand, and it continuously evaluates and adjusts to nuances and subtleties of consumer behaviour far greater than has ever been understood, let alone appreciated in terms of revenue potential.

However, we anticipate that these varied perspectives on the potential of AI will converge as AI becomes a crucial component of a successful and enduring relationship between CPG and its consumers. This will grow more important as both retailers and CPG brands foresee rising expenses in 2024 (63% of CPG leaders and 58% of retailer leaders believe that the costs of materials and the expenses associated with business operations will rise this year). They plan to offset these expenses by charging consumers more.

Creating a collaborative mindset with the consumer in mind

The marketplace has grown wider, as shopping becomes more scattered across various locations and online platforms, and shoppers have greater discernment about the items they purchase – all of which pose difficulties for ecommerce retailers. This situation underscores the necessity for both retailers and CPG manufacturers to maintain a strong connection with their customers. If you don’t understand them, what is relevant now, and bear in mind those needs have changed since you began reading this sentence, you will fail. Only an autonomous AI machine learning hyper-personalisation solution can cope.

Please take the time to review the distinction between the world’s top 30 hyper-personalisation vendors.

We observe CPG vendors still pursuing high sales numbers, but what happens when sales dip? Are they still measuring success accurately? The retailers that have managed to weather the storm over the past years have innovated and remained intensely focused on meeting customer demands; those that failed to do so have disappeared.

In a marketplace so interconnected, achieving success today hinges on embracing open, cooperative, and flexible ways of thinking and operating – by utilising each other’s strengths and innovations to face the future confidently. In the end, it’s essential to keep a deep understanding of the consumer. By doing what’s best for the consumer, the entire marketplace benefits.